%20(1).svg)

.svg)

Introduction

When you start looking at buying rural property, understanding farmland loans is one of the most practical steps you can take. This guide is written for landowners and farmers who want clear, usable information about lending options, what lenders expect, and how to protect soil and long term value. It focuses on real choices and trade offs, with examples you can use when comparing a farm purchase loan or exploring farm land financing in Canada.

What are farmland loans?

Farmland loans are mortgages or secured loans made to buy agricultural land, to refinance existing farm property, or to improve farm infrastructure. Lenders look at the land value, the operation's cash flow, and the borrower’s experience and equity. These loans can finance bare acreage, a working farm, or a farmstead with buildings and equipment.

How do farm land loans work?

Most farm land loans work like other mortgages, but they come with sector specific considerations. Lenders can require different down payments, longer amortizations for the land or shorter amortizations for buildings, and may base lending decisions on farm income rather than salaried income. If you choose a farm purchase loan, the process typically includes appraisal, title review, and proof of income or farm projections.

How to get farm land loans?

To get a farm land loan, prepare to show a clear plan and the documents lenders ask for. New buyers and beginning farmers can qualify, but they must demonstrate a realistic repayment plan. Start with a lender who understands agriculture, like regional farm credit institutions, commercial banks with farm divisions, or specialty lenders focused on rural property.

Qualifying and documents lenders ask for

When qualifying for an agricultural land loan, lenders primarily look for financial stability and a clear ability to repay the debt. While specific requirements can vary between institutions, preparing a standard set of documentation beforehand is a practical way to reduce delays and demonstrate your seriousness as a borrower.

To ensure a smooth application process, you should assemble identification and ownership documents for all parties involved, along with recent tax returns and comprehensive farm financial statements. Additionally, lenders will typically request projected farm budgets or cash flow statements, the purchase agreement or listing information for the property, and full details regarding any existing mortgages, easements, and encumbrances on the land.

What are current farmland interest rates?

Interest rates for agricultural land change with market conditions. Ask lenders for their current farmland interest rates or farm land loan interest rates, and confirm whether those rates are fixed or variable. Typical differences you will see include lower rates for established farmers with strong cash flow, and higher rates for speculative purchases or beginning farmer loans. When comparing offers, look at annual percentage cost, fees, amortization, and prepayment rules.

Comparing farm credit vs bank farm loans

When you compare lenders, think about expertise, flexibility, and the full cost. Farm credit institutions often provide programs tailored to agriculture, including longer amortizations and sector specific advice. Banks may offer competitive farm land mortgage rates but can be less flexible on atypical cash flows. Narrative comparisons are useful: farmland loans vs traditional loans often mean different underwriting rules and different support for farm planning.

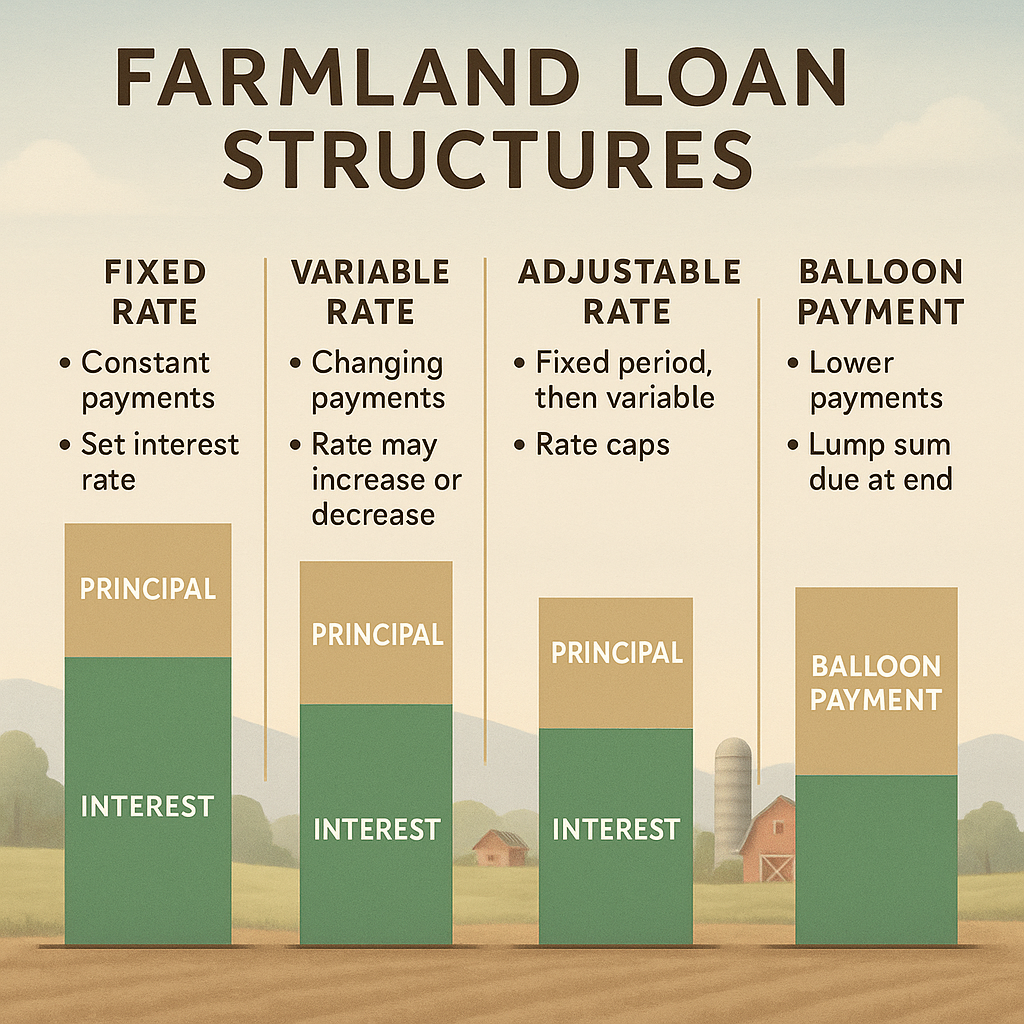

Types of farmland financing and loan structures

There are several common loan types to consider depending on your specific agricultural needs. Choosing a structure that matches your long term plan is a practical way to reduce risk and keep payments manageable throughout the duration of the term. For those looking to acquire property, a long term mortgage for land purchase is a standard option, often amortized over 15 to 25 years to provide stability. Alternatively, short term construction or improvement loans are available for those needing to develop buildings or infrastructure on the land.

For active operations, agricultural operating lines can help manage seasonal cash flow needs, while equity loans or second mortgages allow you to utilize existing farm value for further investment. There are also specialized government backed or subsidized programs designed specifically for beginning farmers or those focused on conservation purchases. By selecting the right financial tool, you can ensure your land remains a productive asset while maintaining the ease and simplicity of your broader financial strategy.

How to qualify for farmland loans and how much you can borrow

Qualification depends on down payment, credit, farm income, and the property itself. Lenders typically expect larger down payments for bare land than for improved property. You can often borrow a higher share of purchase price when the property has established production or reliable rental income. For beginners, loan amounts may be constrained until you build a credit and production history, but there are specialized options under beginning farmer land loans and government partnership programs.

What makes farm land loans different from residential mortgages?

Farm land loans often consider farm business risk, commodity price volatility, and the condition of soil and improvements. Lenders may ask about tenant history if land is leased, crop rotation plans, and stewardship practices because these affect land value over time. A lender that understands agriculture will factor in realistic harvest cycles, off season revenue, and potential conservation programs when setting terms.

Soil responsibilities and long term land care when you borrow

Accepting a loan on farmland usually means you are planning to steward the asset for years. Protecting soil health preserves both productivity and collateral value. Lenders may not require a soil management plan, but having one helps your case and reduces risk. Practical stewardship actions include maintaining ground cover, managing erosion, rotating crops, and planning improvements that reduce long term input needs.

Can I get a loan to buy farmland as a beginner?

Yes, beginners can get a loan to buy farmland, but the path is often different from experienced operators. Lenders commonly require a stronger equity position, a mentor or co-signer, or participation in a beginning farmer program. Look for lenders who offer specific programs for new entrants and be ready to present a credible business plan and farm budget.

How to compare farm loan rates and choose a lender

Comparing farm loan rates involves more than picking the lowest rate. Consider amortization terms, prepayment penalties, fees, and how the lender treats farm income variation. When you review offers, compare the effective cost and flexibility. For example, a slightly higher farm land loan rates offer that permits penalty free prepayment might save you money if you plan to pay down principal quickly. Tools, spreadsheets, and lender conversations help, and services like Land4Rent can support clear lease terms when land will be rented rather than farmed directly.

What documents are needed for farm loans?

Most lenders ask for title information, personal identification, tax returns, business financials, and a purchase agreement. If the land is rented, provide lease agreements. If you already operate a farm, include production records and balance sheets. Clear documentation speeds approvals and improves negotiation leverage.

How long do farmland loans take to close?

Closing time varies by lender, appraisal availability, and complexity of title issues. A straightforward refinance or a purchase with clear title can close in a few weeks. More complex deals, including those with environmental review or multiple owners, can take several months. Build time into your schedule and follow up actively on outstanding items.

Can I refinance farm land loans?

Refinancing is common when rates change, when you want to change amortization, or to access equity for improvements. Before refinancing, compare costs like appraisal fees and any prepayment penalties to the savings from lower farmland mortgage rates. If you refinance to consolidate debt, be careful not to stretch repayment beyond what the farm cash flow can support.

Practical steps to apply for a farm purchase loan

Start with a pre-application and a lender conversation. Collect your documentation, get a realistic budget for the property, and ask for a written estimate of costs and terms. Visit multiple lenders, and ask for details on the loan type, amortization, interest treatment, and any required farming experience. If you plan to lease land, formalize lease terms so the lender can evaluate rental income as part of your application. Tools like Land4Rent help make lease responsibilities clear and professional, which lenders appreciate.

Managing farmland loans over the long term

Once you have financing, managing the loan means managing risk. Keep clear financial records, set aside reserves for crop failures and weather events, and maintain the land so it retains value. Plan capital improvements in phases so debt does not outpace revenue. Consider insurance for structures and business interruption. Regular conversations with your lender can uncover options for restructuring if your business changes.

Conclusion

Financing a farm or acreage is a long term commitment that blends financial planning with land stewardship. Whether you choose a traditional bank, a farm credit institution, or a specialty lender, focus on realistic budgets, clear documentation, and practices that protect land value. Comparing farm land lenders on more than just rate will yield better outcomes. If you plan to lease land, keep lease terms professional and transparent; tools like Land4Rent can help structure those arrangements so both owners and operators understand their responsibilities.

Frequently Asked Questions (FAQs)

What are farmland loans?

Farmland loans are mortgages or secured loans used to buy, improve, or refinance agricultural land and related assets, with terms that reflect farm risks and income cycles.

How to get farm land loans?

Prepare financial records, a purchase agreement, and a farm budget, then apply to lenders experienced in agriculture, including farm credit institutions and specialized bank divisions.

What are current farmland interest rates?

Rates change with market conditions and borrower risk; request current farmland interest rates from multiple lenders and compare effective costs, not just headline rates.

Can I get a loan to buy farmland as a beginner?

Yes, beginners can qualify but may need larger down payments, a mentor or co-signer, and a solid business plan to show repayment ability.

What documents are needed for farm loans?

Lenders typically want ID, tax returns, business financials, a purchase agreement, title documents, and leases or production records when available.

How long do farmland loans take to close?

Closing can take a few weeks for straightforward deals and several months for complex transactions involving environmental or title issues.

What makes farm land loans different from residential mortgages?

Farm loans consider agricultural income cycles, production risks, soil and stewardship, and sometimes different amortization or covenants based on farm realities.

Can I refinance farm land loans?

Yes, refinancing is common to access equity, improve terms, or consolidate debt, but consider fees and any prepayment penalties before proceeding.

How to compare farm loan rates?

Compare interest rates, amortization, fees, prepayment terms, and lender flexibility, and model scenarios to see the true cost across the loan life.

Why choose farm credit for land loans?

Farm credit institutions often offer agriculture specific programs, sector knowledge, and flexibility that align with the seasonal and capital needs of farming operations.

.svg)

.svg)